|

|

[转贴] 收集:Healthy balance sheets? They owe $7.2 trillion, the most ever

本帖最后由 not4weak 于 2010-9-3 19:49 编辑

Commentary: Healthy balance sheets? They owe $7.2 trillion, the most ever

You may have heard recently that U.S. companies have emerged from the financial crisis in robust health, that they've paid down their debts, rebuilt their balance sheets and are sitting on growing piles of cash they are ready to invest in the economy.

You could hear this great news pretty much anywhere — maybe from Bloomberg, which this spring hailed the "surprising strength" of corporate balance sheets. Or perhaps in the Washington Post, where Fareed Zakaria reported that top companies "have accumulated an astonishing $1.8 trillion of cash," leaving them in the best shape, by some measures, "in almost half a century."

Or you heard it from Dallas Federal Reserve President Richard Fisher, who recently said companies were "hoarding cash" but were afraid to start investing. Or on CNBC, where experts have been debating what these corporations are going to do with all their surplus loot. Will they raise dividends? Buy back shares? Launch a new wave of mergers and acquisitions?

(又是玩心理战?历史已经说明,这一次很可能不同了)

It all sounds wonderful for investors and the U.S. economy. There's just one problem: It's a crock.

American companies are not in robust financial shape. Federal Reserve data show that their debts have been rising, not falling. By some measures, they are now more leveraged than at any time since the Great Depression.

(目前大多数拖延银行贷款的,最后都被SHORT SALE或FORECLOSED了,债太高了.)

You'd think someone might have noticed something amiss. After all, we were simultaneously being told that companies (a) had more money than they know what to do with; (b) had even more money coming in due to a surge in profits; yet (c) they have been out in the bond market borrowing as fast as they can.

Does that sound a little odd to you?

A look at the facts shows that companies only have "record amounts of cash" in the way that Subprime Suzy was flush with cash after that big refi back in 2005. So long as you don't look at the liabilities, the picture looks great. Hey, why not buy a Jacuzzi?

According to the Federal Reserve, nonfinancial firms borrowed another $289 billion in the first quarter, taking their total domestic debts to $7.2 trillion, the highest level ever. That's up by $1.1 trillion since the first quarter of 2007; it's twice the level seen in the late 1990s.

The debt repayments made during the financial crisis were brief and minimal: tiny amounts, totaling about $100 billion, in the second and fourth quarters of 2009.

Remember that these are the debts for the nonfinancials — the part of the economy that's supposed to be in better shape. The banks? Everybody knows half of them are the walking dead.

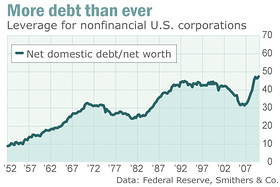

Central bank and Commerce Department data reveal that gross domestic debts of nonfinancial corporations now amount to 50% of GDP. That's a postwar record. In 1945, it was just 20%. Even at the credit-bubble peaks in the late 1980s and 2005-06, it was only around 45%.

The Fed data "underline the poor state of the U.S. private sector's balance sheets," reports financial analyst Andrew Smithers, who's also the author of "Wall Street Revalued: Imperfect Markets and Inept Central Bankers," and chairman of Smithers & Co. in London.

"While this is generally recognized for households," he said, "it is often denied with regard to corporations. These denials are without merit and depend on looking at cash assets and ignoring liabilities. Cash assets have risen recently, in response to the fall in inventories, but nonfinancials' corporate debt, whether measured gross or after netting off bank deposits and other interest-bearing assets, is at peak levels."

By Smithers' analysis, net leverage is nearly 50% of corporate net worth, a modern record.

There is one caveat to this, he noted: It focuses on assets and liabilities of companies within the United States. Some U.S. companies are holding net cash overseas. That may brighten the picture a little, but the overall effect is not enormous, and mostly just affects the biggest companies.

That U.S. companies are in worse financial shape than we're being told is clearly bad news for those thinking of investing in U.S. stocks or bonds, as leverage makes investments riskier. Clearly it's bad news for jobs and the economy.

But why is this line being spun about healthy balance sheets? For the same reason we're told other lies, myths and half-truths: Too many people have a vested interest in spinning, and too few have an interest in the actual picture.

Journalists, for example, seek safety in numbers; there's a herd mentality. Once a line starts to get repeated, others just assume it's correct and join in.

Wall Street? It's a hustle. This healthy balance-sheet myth helps sell stocks and bonds. How many bonuses do you think get paid for telling customers the stark facts, and how many get paid for making the sale?

You can also blame our partisan age too. Right now, people on the right have a vested interest in claiming businesses are in healthy shape. That makes the saintly private sector look good, and demonizes President Barack Obama and Big Government for scaring away investment. Vote Republican! Meanwhile, people on the left have an interest in making businesses sound really healthy too: If greedy companies are hoarding cash instead of hiring people, they can cry "Shame on them! Vote Democratic!"

As ever, the truth is someone else's problem and no one's responsibility.

When it comes to the economy, let's just hope the public is too hopped up on painkillers and antidepressants to notice. If they knew what was really going on, there'd be trouble |

|

发表于 2010-9-3 19:26

|

发表于 2010-9-3 19:26

|

发表于 2010-9-3 19:31

|

发表于 2010-9-3 19:31

|  阅过

阅过